VTI and VUG: A Two ETF Portfolio for Long-Term Wealth Building

In a world of complexity, sometimes the most powerful investment strategies are also the simplest ones.

The investing landscape is filled with seemingly endless investment avenues. Financial advisors push complex investment portfolios filled with proprietary mutual funds. Social media is pushing the latest great idea. /rwallstreetbets is pushing the next meme stock.

Despite all of the madness surrounding investing, this blog displays how simplicity can prevail. By combining just two Vanguard ETFs (or the similar from other brokerages), one can potentially deliver institutional-quality diversification and growth-oriented returns that rival far more complicated strategies.

But before you dismiss this as overly simplistic, consider this: some of the most successful long-term investors swear by streamlined approaches. Many famous investors including Warren Buffett, John Bogle, and Burton Malkiel all recommend simple S&P 500 funds.

The VTI/VUG combo I use as the backbone of my personal portfolio takes this concept one step further, adding a growth tilt while maintaining the core principle of broad market exposure.

Meet Your Investment Duo

VTI: Your Market Foundation

The Vanguard Total Stock Market Index Fund ETF (VTI) is like owning a slice of corporate America. This single fund provides exposure to nearly 4,000 U.S. stocks. Everything from tech behemoths like NVIDIA and Amazon down to small-cap companies you've never heard of but that might become tomorrow's success stories.

The top 5 holdings are as follows:

Microsoft Corp. (MSFT) – 6.19%

NVIDIA Corp. (NVDA) – 6.13%

Apple Inc. (AAPL) – 5.13%

Amazon.com Inc. (AMZN) – 3.15%

Facebook Inc. (META) – 2.68%

VTI is cap weighted, meaning the larger companies comprise a greater proportion of the fund. To no surprise, large cap stocks (>$10B) comprise most of the fund.

VTI Morningstar Equity Style Box

Over the past decade, VTI has delivered annualized returns nearing 13%.

VTI’s advantage is the ability to have a share of over 4,000 stocks with a single ETF. This is instant diversification across every sector of the U.S. economy. Everything from technology to financials to health care to consumer goods. They are all represented in proportion to their market value.

VUG: Your Growth Accelerator

The Vanguard Growth Index Fund ETF (VUG) takes a more focused approach, concentrating on U.S. companies that exhibit growth characteristics. Think higher price-to-earnings (P/E) ratios, strong earnings growth, and expanding market opportunities. With less than 200 holdings (165 the day I write this) and an expense ratio of 0.04%, VUG provides targeted exposure to the companies driving innovation and expansion in the American economy.

VUG's top holdings are the ballers of the business world:

Microsoft Corp. (MSFT) – 11.76%

NVIDIA Corp. (NVDA) – 11.63%

Apple Inc. (AAPL) – 9.71%

Amazon.com Inc. (AMZN) – 6.53%

Facebook Inc. (META) – 4.57%

Look familiar? These are the same top 5 holdings as VTI, but double the weight.

The fund is heavily weighted toward technology (about 60% of holdings) and consumer discretionary stocks (about 19% of holdings), sectors that have historically driven market outperformance during growth cycles. As you can see, big companies looking to continue expanding.

VUG Morningstar Equity Style Box

Over the past decade, VTI has delivered annualized returns nearing 16%.

While VUG has delivered impressive returns, it experiences significant volatility along the way. When growth stocks fall out of favor, VUG experiences sharper declines than more diversified funds.

The Strategic Advantages

The beauty of pairing VTI and VUG lies in their complementary nature. Some say overlap, but because this is my blog, I say complimentary nature. VTI gives you the entire U.S. stock market, ensuring you don't miss out on value opportunities or defensive sectors. VUG adds a deliberate tilt toward the growth companies that have historically driven long-term wealth creation.

During my short investing career, growth stocks have massively outperformed, so I have a natural affinity towards them.

Together, these funds provide exposure to both growth and value segments of the market. Everything from large, well established blue-chips alongside emerging innovators. I’m essentially getting the benefits of a sophisticated institutional portfolio without the complexity or high fees.

Cost Efficiency That Compounds Over Decades

John Bogle’s threshold for fees is an expense ratio of 0.2. Anything above this and fees eat away at your true returns. We can thank Bogle for founding Vanguard and the popularization of low-cost funds.

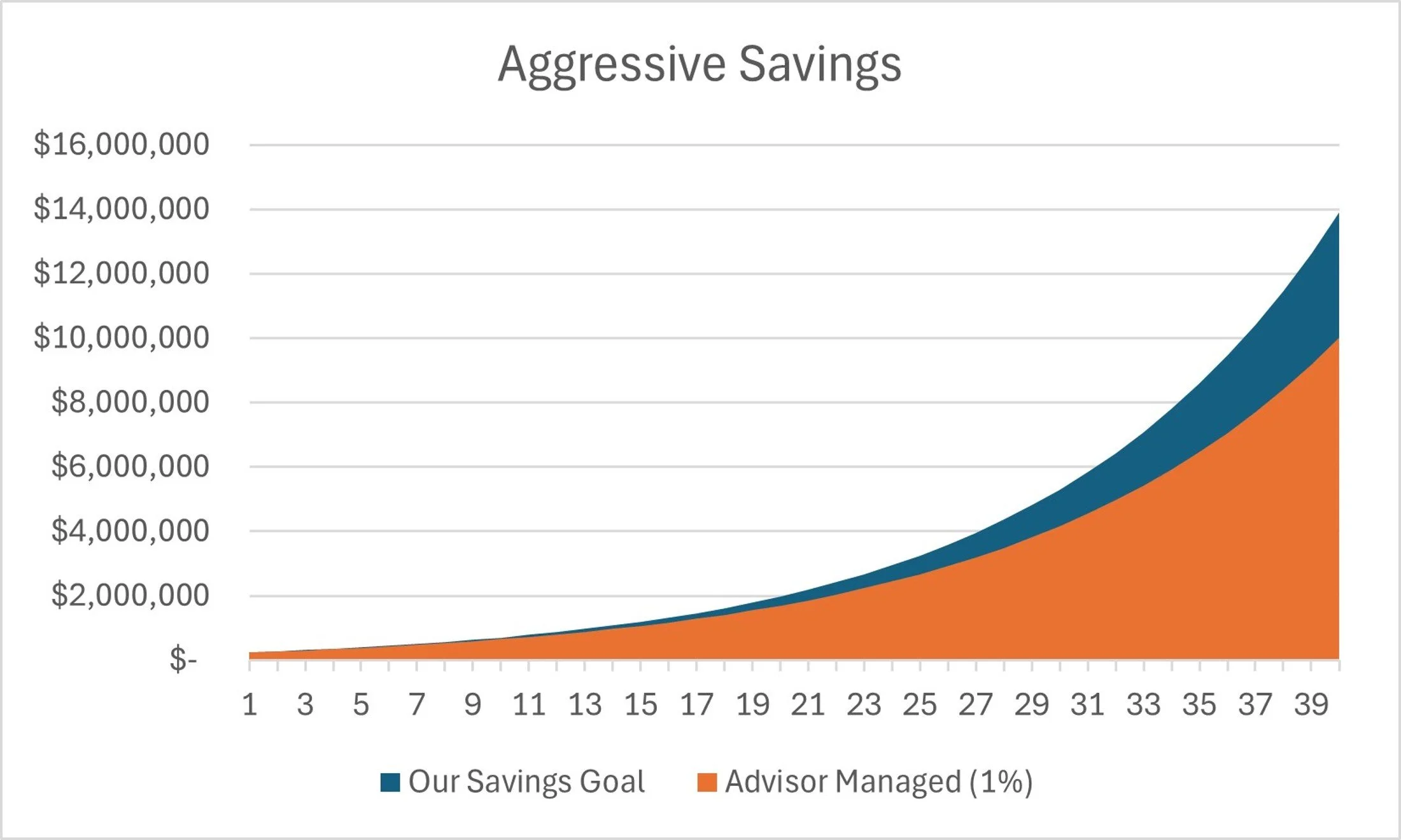

VTI and VUG have expense ratios of 0.03% and 0.04% respectively. I’m paying less than $4 annually per $10,000 invested. Vanguard makes their money from volume, not by margin. Compare this to the typical actively managed mutual fund charging 0.75-1.50% annually. Maybe an advisor charging an additional 1%. The math becomes compelling quickly.

For the disciplined buy-and-hold investor, fees will cost you millions. In my simulation, 1% would cost me $4M over 40 years.

Simplicity Eliminates Decision Making

Choosing between 1 of 2 ETFs is far simpler than choosing between 4,000 stocks on the U.S. exchange. Simplicity increases adherence to the plan. A plan that involves dollar-cost averaging into a low-cost, passively managed index fund every week. Market highs or market lows, I’m investing every Monday.

Tax Efficiency

As someone in their peak earning years, I would rather see investments grow via capital appreciation rather than dividend payments. VTI and VUG have dividend payments of 1.5% and 0.5% respectively. It is logical that VUG has a lower dividend as the companies are looking to reinvest maximally to facilitate expansion.

The ETF structure also allows for tax-efficient in-kind redemptions, and the broad diversification means lower portfolio turnover compared to actively managed alternatives. For taxable accounts, this tax efficiency can add meaningful value over time.

Potential Drawbacks to Consider

The U.S.-Only Limitation

Perhaps the most significant limitation of a VTI/VUG strategy is its complete focus on U.S. markets. I’m missing exposure to international developed markets and emerging economies that might outperform U.S. stocks in certain periods. One of those periods being early to mid-2025 where U.S. funds have underperformed global funds.

Historically, international diversification has provided risk reduction benefits, even if it hasn't always enhanced returns. Over the past decade, Vanguard’s Total World Stock ETF (VT) achieved an average annual return of 10%. That might not sound like a big difference, but here is the math.

ETF Comparison - VT, VTI, VUG

Yeah…3% annually is a lot. 6% is a game-changer. Had you invested in VUG vs VT, your portfolio would have grown to almost twice the portfolio size -- 2.5x vs 4.4x. Pretty significant. However, markets are cyclical. Everyone has their day in the sun. With current economic policies, I wouldn’t be surprised if international funds outperform U.S. growth funds. They are due.

Will it be enough to make up for the many years of underperformance? Time will tell.

Growth Concentration Risks

Both VTI and VUG are cap weighted. VUG’s heavy concentration in growth stocks means I’m essentially doubling down on a small number of large cap stocks, particularly technology companies. This creates sector-specific risks.

Note these funds are self-cleansing meaning compositions change as company market caps change. There have been eras when financials, consumer discretionary, and industrials have made up significant portions of the fund. It hasn’t always been tech.

VUG’s top 10 holdings represent about 60% of its total assets, meaning your portfolio's performance becomes heavily dependent on a relatively small number of mega-cap stocks.

During growth stock corrections—like the tech selloff in early 2022 and April 2025—VUG can experience dramatic declines. Those who opt for VUG need to be comfortable with this volatility and avoid the temptation to panic-sell during downturns.

Overlapping Holdings Create Concentration

There's significant overlap between VTI and VUG's top holdings. The big dogs, such as the Magnificent 7, appear prominently in both funds, creating significant concentration risk.

This overlap limits the diversification benefit supplied by VTI. These appear to be two separate index funds, but the overlap is essentially a leveraged bets on the largest U.S. growth companies -- and I want it that way.

No Defensive Positioning

A VTI/VUG portfolio offers no exposure to bonds, real estate, commodities, or other asset classes that might provide stability during equity market downturns. During bear markets, both funds will likely decline together (VUG more significantly), offering little downside protection.

Risk-averse investors or those nearing retirement might find this lack of defensive positioning uncomfortable, especially during extended market corrections. Despite infrequency since 2008, bear markets represented by a 20% market decline from the peak occur every 3-4 years and last about 1 year.

Optimal Allocation Strategies

The 70/30 Foundation

If I were asked my recommendation as to balancing VTI and VUG, I’d say a reasonable starting point is allocating 70% to VTI and 30% to VUG. This approach maintains broad market exposure while adding a meaningful growth tilt. Historical backtesting suggests this allocation has provided attractive risk-adjusted returns over long periods.

The 70/30 split ensures that your portfolio doesn't become too concentrated in growth stocks while still allowing you to participate in the outperformance that growth companies have historically delivered. During market corrections, VUG is a rollercoaster pointing towards the ground. A pure VUG portfolio makes for a ride too steep for most. I’m thinking the 2000 dot com bubble.

Age-Based Adjustments

As an investor in my early 30’s, I have a long investment horizon. I could be holding these investments for the next 50 to 60+ years. Crazy to think about.

During recent market corrections, I lean on VUG far more than VTI. This spring, I was buying VUG week after week, but have since resumed investing in a mix of the two.

It’s reasonable for those with decades of investing to consider higher VUG allocations simply because they are living off earned income, not their portfolios. The effects of market pullbacks and downturns are negated by having earned income that supports your burn. Minimal sequence of returns risk.

Growth ETFs are reasonable, if not encouraged, during the wealth accumulation phase. As you approach retirement, gradually shifting toward a higher VTI allocation can provide more stability and broader diversification. Accumulation becomes maintenance.

Real-World Implementation

The beauty of this strategy lies in its low maintenance requirements. Complexity leads to analysis paralysis. I have two index funds to choose from. On any given Monday, I just pick one. I hoard VTI and VUG. Buy-and-hold forever – or at least until I need to cover living expenses during retirement.

Take a look at your ratio of VTI/VUG every 6 or 12 months. Rebalance if needed. I don’t mean sell one to buy the other, just purchase the one you feel you need more of in your life. There are places to stress, this isn’t one of them.

Who Needs the VTI/VUG Combo?

This two-ETF approach is ideal for long-term investors with at least 10-year time horizons who want equity diversification without complexity. I recommend it to the following:

Those self-managing their retirement accounts

Those looking for one-click diversification

Those looking for a simple, long-term investing solution

Those looking to minimize fees or replace a financial advisor

Those who struggle with analysis paralysis

Alternative Considerations

Before committing fully to VTI and VUG, consider whether you need additional diversification. Adding international exposure through VT which reduces U.S.-specific risks. International funds have historically underperformed U.S. funds, but past performance does not guarantee future returns.

Those approaching retirement should opt for VTI, but also consider adding some fixed income productions. Something like a Total Bond Market Fund ETF (BND). This minimizes volatility, which is beneficial as one becomes reliant on their portfolio to support living expenses. This comes at the cost of growth which is acceptable after finding yourself firmly in the “maintaining wealth” phase. It would just be a matter of adding BND a few year prior to retirement.

For ultimate simplicity, some investors might prefer holding just VTI alone, accepting market returns without the additional growth tilt. No pushback from me.

Building Wealth Through Simplicity

The VTI/VUG combination is my way of finding a middle ground between a simple broad market U.S. fund and the disgusting complexity of former advisor’s portfolio.

Lessons learned. As always, my blog entries are for educational purposes only, not investing advice. They represent what I do and why I do it.

By focusing on two high-quality, low-cost funds, I have a portfolio that captures the growth potential of American capitalism while maintaining the discipline that long-term wealth building requires.

The key to success with this strategy isn’t perfect market timing or complex optimization. It comes down to consistent execution over long periods. Choose your fund(s), invest regularly, rebalance periodically, and never sell.

The best investment strategy is one you actually commit to. The one that passes the “sleep at night” test. The one you can stick with through various market cycles. If this two-fund approach helps you maintain discipline and avoid behavioral mistakes, it may well outperform more sophisticated strategies that tempt you to tinker and second-guess.

Building wealth isn't about perfection but rather finding a good portfolio and having the discipline to let compound growth work its magic over decades. For many investors, VTI and VUG provide exactly that combination of quality, simplicity, and growth potential that turns steady savers into wealthy retirees.

Best of luck with your investing. Thanks for reading !